Hopefully, you didn’t notice, but the end of 2018 presented such a market.

You might have come across headlines NBR such as this one:

“The stock market is on pace for its worst December since the Great Depression.”

Now that sounds pretty scary. Here‘s another one:

“Are you ready for the financial crisis of 2019?”

You might be surprised to know that the 2019 Q1 return for the S&P 500 was +13.65% (USD). Hardly a crisis.

And that’s the trouble with headlines. News headlines are meant to sell papers and advertising space. Even in our part of the world, doom has been forecast for a while. We’ve learned to be cynical.

When markets do fall, though, it’s very natural for any investor to get nervous.

So, in this article, we thought we would remind you of the reasons why we will never suggest you sell your shares before or during down markets.

- Buying high and selling low just doesn’t make sense. We avoid it at all costs. We can’t really think of a worse reason to sell than the fact that the price went down. Can you?

- Often the money you invest with us is being put aside for very long term goals stretching out 20 or 30 years. Did you know the worst consecutive 20-year return for the S&P 500 over the last 50 years (a time period that included the GFC) was that the value of shares tripled? And that in the worst period over the last 30 years, the total return was over 1,300%?

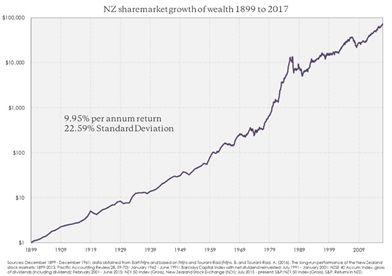

- Looking at New Zealand shares since 1899, average returns were 9.95% per annum. One dollar returns tens of thousands of dollars before taxes and inflation. There’s almost no possible way to mess this up…unless you try to time the market.

- We’ve already factored temporary drops into your plans. When we recommend a portfolio, we know full well there will be up and down markets. When determining if your portfolio will achieve your goals, we count on down markets. Frankly, if we don’t get down markets, you’ll so overwhelmingly overshoot your financial goals that we’ll need to have other conversations. So, if temporary down markets come, your first instinct should be, “my adviser already factored this in”, because we have.

- If you really need the money and your time horizon is short, you will already have a substantial position in cash and bonds that have far more stable prices than shares. And that’s not by accident.

- We would have recommended that portfolio because we knew you would need the money over the shorter term.

- We monitor your plan regularly as we meet with you. If you need to do something to get back on track, we’ll tell you. That’s our job. If necessary, our advice will likely be some combination of saving more, spending less, increasing shares in your portfolio, reducing estate plans, or something else depending on the point you’re at in life. All those things, you can control. The markets, you cannot.

- We’ve built a margin of safety into your plan because we generally calculate on the market delivering a rate of return lower than what we actually expect. This margin of safety gives you flexibility during downtimes to ride it out, without your plans being negatively impacted.

- We’re not aware of any credible academic evidence (and we’ve looked) that suggests there is a methodical way to time markets. Without evidence, you are left with hunches and guesses. We don’t manage money based on hunches and guesses.

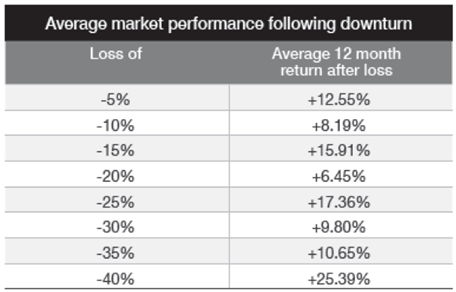

- The past gives us a rich understanding of markets. One question we can ask is, after the market has fallen X amount, what is the median return over the next 12 months? As you can see below, the data never allows you to comfortably say the market is ‘falling’. You can only know the market has ‘fallen’ (past tense), because the majority of cases after it has fallen, it has subsequently risen.

The reality is that after markets have fallen, not only are we unlikely to tell you to sell shares (short of you needing the money for a specific purpose), but we are likely to tell you to buy shares.

We do this with our normal rebalancing exercise. If, for example, your portfolio is 60% shares and 40% cash and bonds, when shares fall in value the ratio will change. Perhaps it tips closer to 55%/45%. When that happens, we sell down bonds and cash in order to purchase shares and rebalance the portfolio back to its target ratio.

We know that when markets have fallen like they did in the last quarter of 2018, it can feel like a cause for concern. But we also want you to know that it’s our job to be concerned for you. Down markets are inevitable. When they do occur, our advice will be there to keep you on track, but our real hope is that you have a sense of peace knowing we’ve already factored these markets into your plans.